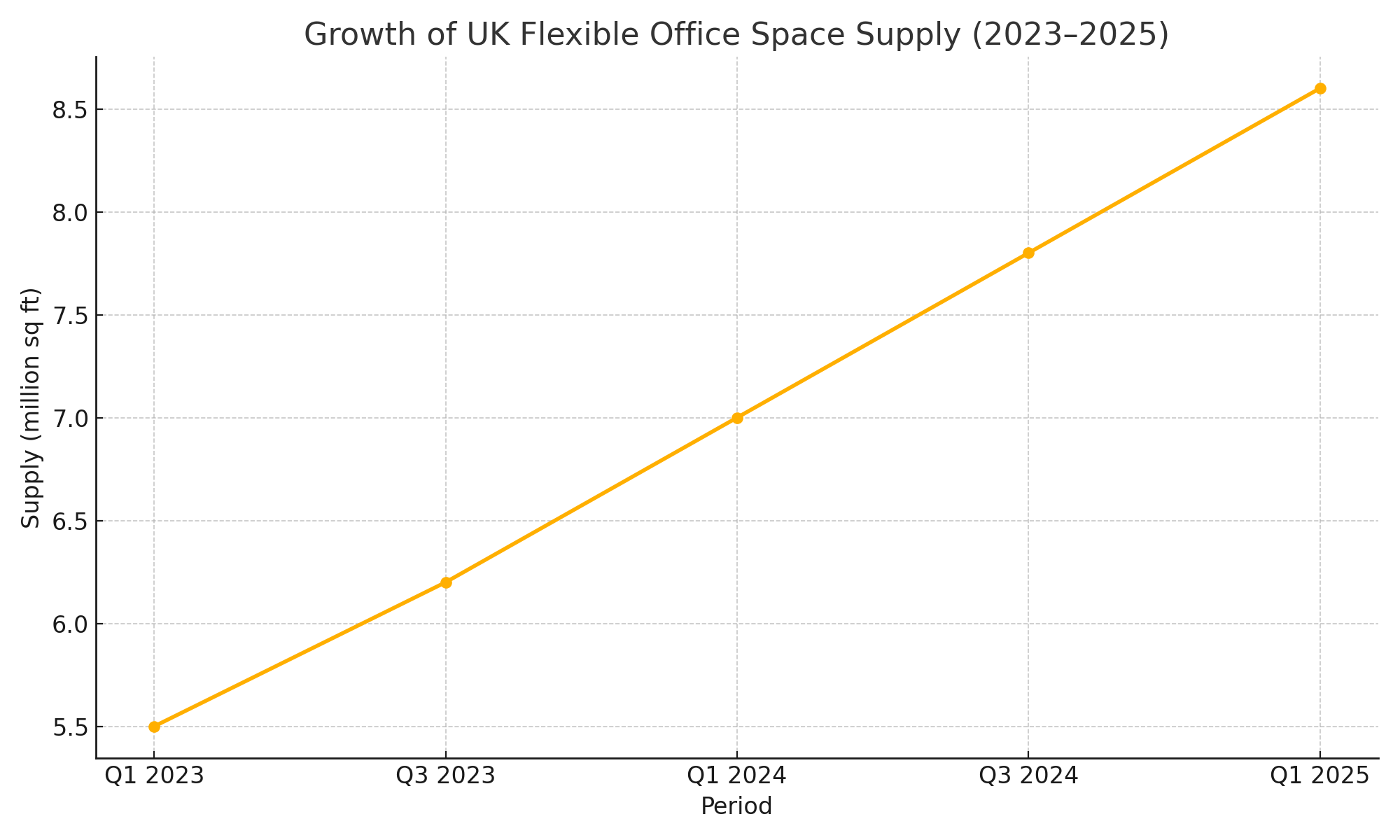

The London office market saw a strong start to 2025, with leasing activity rebounding and clear signs of a “flight to quality” among occupiers. In the first two quarters of the year, companies actively secured high-quality office space, even as overall vacancy remained elevated compared to pre-pandemic levels. At the same time, the flexible and serviced office sector is booming, with available flex space increasing by more than 30% year-on-year. Both tenants and landlords are embracing more agile workspace solutions.

Market Overview: Strong Leasing and Investment Rebound

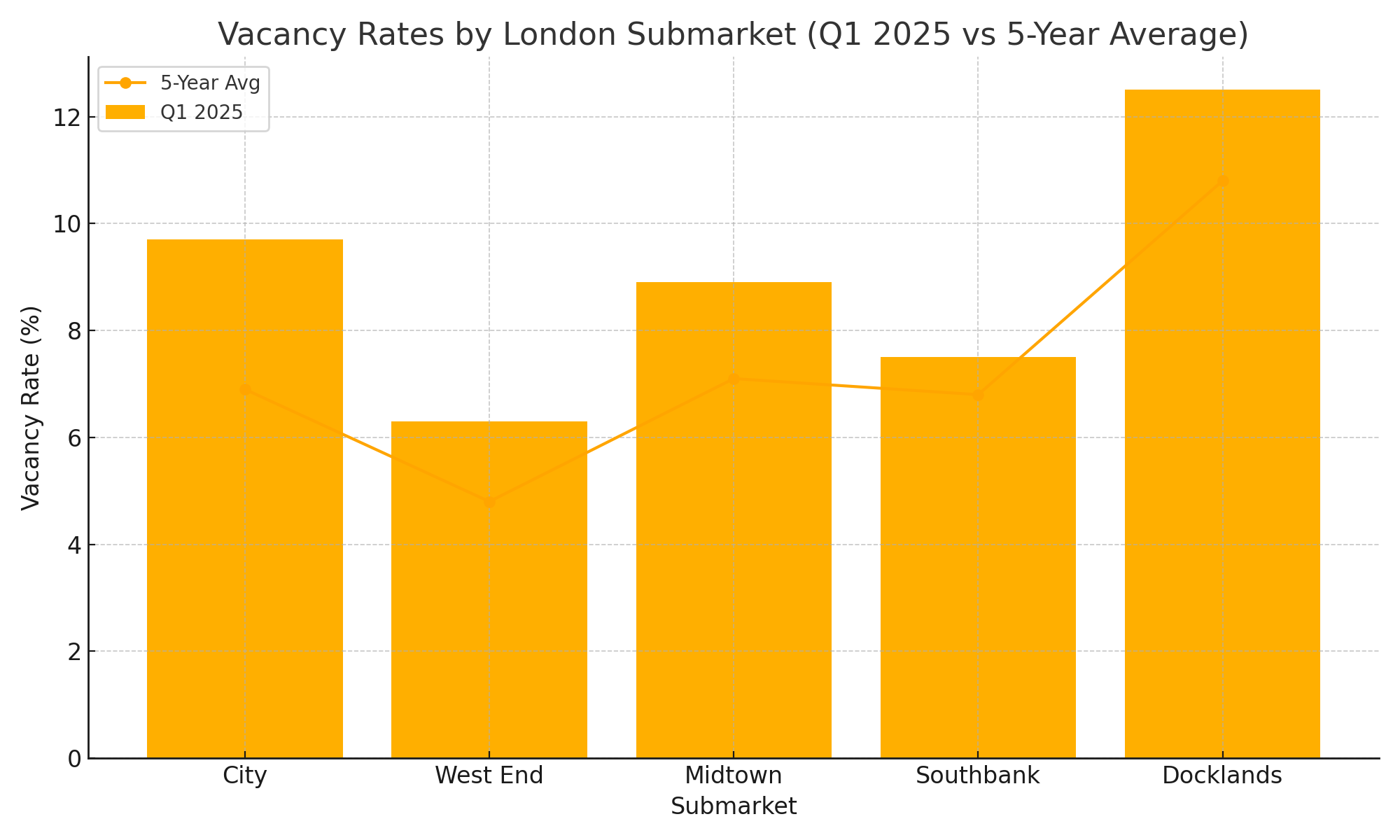

Following a slower end to 2024, office leasing in London picked up momentum in Q1 2025. Central London office take-up reached approximately 2.1–2.4 million sq ft, roughly in line with the ten-year average. Across all London submarkets, including the City, West End, Midtown, Southbank and Docklands, take-up totalled 3.11 million sq ft in Q1, a 27.5% increase quarter-on-quarter.

In Q2, take-up remained strong, particularly in the City core and West End, where ESG-compliant new builds and refurbishments attracted significant interest.

The Shift Towards Quality Office Space

Occupiers are showing a clear preference for Grade A space in prime locations. This trend, often referred to as the “flight to quality,” is especially evident in demand for BREEAM-rated buildings with high EPC scores, employee wellness amenities, and strong transport connections.

Vacancy Rates: A Two-Speed Market

While demand for top-tier space is high, London’s overall office vacancy remains elevated. The City recorded a 9.7% vacancy rate in Q1, while the West End stood at 6.3%. However, this is not evenly distributed: new and refurbished buildings are seeing high absorption rates, while older, lower-spec stock struggles to find tenants.

Serviced and Flexible Office Growth

The flexible office market continues to surge. Available flex space increased over 30% year-on-year, driven by:

- Growing demand for hybrid work models

- An influx of new entrants and expansion by major providers

- Landlords launching their own managed workspace offerings

Operators like Fora, Huckletree, and x+why are rapidly expanding in both Central and fringe markets. Landlords, too, are increasingly offering turnkey fit-outs or partnering with flex providers to meet evolving occupier needs.

Rents and Incentives

Prime office rents remained firm in Q1 and Q2 2025:

- City Core Grade A rents reached £77.50 per sq ft

- West End Grade A rents rose to £130.00 per sq ft in some locations (e.g. Mayfair and St James’s)

- Midtown Grade A rents stood at £82.50 per sq ft

Incentives such as rent-free periods remain in place, typically 21–24 months on 10-year leases, but are decreasing slightly in high-demand locations.

Submarket Highlights

City of London

- Q1 take-up: approx. 1.2 million sq ft

- Driven by financial services, legal, and insurance sectors

- Demand focused on new developments like 100 Leadenhall and 2 Aldermanbury Square

West End

- Q1 take-up: around 970,000 sq ft

- Mayfair and Soho are hotspots for media, private equity, and family offices

- Premium buildings with wellness features are leasing fastest

Midtown

- Strong activity from professional services and creative industries

- Rents holding steady despite wider vacancy

- Major pre-lets in developments around Holborn and Farringdon

Southbank & Docklands

- Southbank sees steady leasing due to riverside appeal and proximity to Waterloo

- Docklands struggles due to remote feel and lack of new ESG-compliant buildings

ESG and Refurbishment Focus

Landlords are under pressure to upgrade ageing assets. Tenants increasingly require EPC B-rated buildings or better. Refurbishments with strong ESG credentials, such as smart systems, cycle facilities, biophilic design, and sustainable materials, are outperforming the market.

Investment Market Reawakening

After subdued activity in late 2024, Q1 2025 saw over £2.4 billion in office investment transactions in London. Overseas investors, especially from Asia and the Middle East, have shown renewed appetite for core assets.

Deals of note include:

- A £450 million acquisition in the City by a Singaporean REIT

- South Korean fund entering a JV for a West End development

- A major pension fund acquiring a BREEAM Outstanding scheme in Midtown

Outlook for Second Half of 2025

The second half of 2025 is expected to continue building on this momentum:

- Hybrid working will remain dominant, with firms optimising for less space, but higher quality

- Demand will continue to focus on sustainable, flexible, and well-connected buildings

- Landlords with Grade B or C stock may face increased pressure to refurbish or repurpose

Flex space will play a growing role in portfolios, especially among SMEs and global firms establishing hub-and-spoke models.

Find Office Space in London That Matches Your Business Goals

Whether you're looking for a sustainable HQ in the City, a boutique office in Mayfair or a flexible workspace in Midtown, now is the time to secure a space that reflects your company’s future. With demand rising for high-quality offices, exploring your options early can help you stay ahead in a competitive market. Browse a wide range of serviced, managed and leasehold offices across London, available now to suit teams of all sizes and industries.